Palantir's Road to $100

Palantir's Q4 earnings report showed 70% growth in its U.S. commercial business, and the company raised its 2024 forecast.

The Palantir-Oracle partnership is expected to drive international commercial and government growth.

Palantir's Q1 earnings could exceed expectations, and the stock looks poised for further gains despite potential turbulence in the near term.

I am keeping my year-end/early 2025 price target in the $35-$45 range, and Palantir's stock could reach $100 by 2030.

Palantir's stock rose 24% in the following session (the day after the report).

Here's why: Palantir's U.S. commercial business, now the company's crown jewel (not the government segment anymore), grew by a staggering 70% in Q4. This was a sharp increase from the mid-20% growth we saw several quarters ago when the economy was going through a challenging phase and before the "AI revolution" shifted into high gear.

I'm not much of a soccer player (I prefer "American" football), but if Palantir is "the Lionel Messi of AI," I'm going to own this stock for the long haul. And there is good reason to. Just look at what the company did last quarter.

In addition to beating Q4 sales expectations and illustrating stellar U.S. commercial growth, Palantir's U.S. customer count grew by 55% YoY to 221 customers in Q4. Total commercial contract value rose 107% YoY to $343M during the period. Palantir also raised its 2024 full-year revenue forecast to $2.65-$2.66B, above the $2.64B consensus estimate.

Now, Palantir is getting set to report Q1 earnings early next month, and I think the company can beat its likely sandbagged forecast of $612-$616M in sales. Additionally, Palantir could raise its previous full-year guidance due to its recently announced lucrative Oracle (ORCL) partnership and other bullish developments likely to increase sales growth and improve profitability in future quarters.

Despite Palantir's seemingly elevated valuation, it remains a top AI stock, often misunderstood and underrated by the market. Therefore, Palantir's stock could appreciate considerably throughout 2024, potentially reaching my $35-$45 price target range by year-end or early 2025.

Technically -

Still An Excellent Time To Buy Palantir

Technically, Palantir's stock became overbought after its previous earnings announcement and subsequent run-up above $27. In early February, the stock's RSI shot up to around 80 on massive volume. After a minor pullback, the stock advanced to the $27-$28 range on lover volume, putting in a "blowoff top" with an RSI peak below 70.

Since the near-term top, we saw an excellent 20% pullback to around $22, and now the stock looks poised to start moving higher again. The RSI, CCI, full stochastic, and other technical indicators suggest that technical momentum is improving, and it's positive that the stock came back down to the 50-day MA.

In a "worst-case" scenario, and only likely if a broad market correction occurs, Palantir's stock could close the gap around the $19-$20 level, resulting in a 25-30% pullback from its recent high. If this scenario occurs, it should lead to an excellent long-term buying opportunity despite the short-term pain.

Not Everybody Is Bullish On Palantir

Recently, Monness downgraded the shares to sell from neutral, citing the company's "rich valuation." The firm has set a $20 price target on the stock, saying that "on the back of an unprecedented generative AI hype cycle, Palantir surged in 2023, and the stock's upward trajectory has continued in 2024, leaving the company with what they view as an egregiously rich valuation."

Considering Palantir's enormous growth and profitability potential, I disagree that the stock has an egregiously rich valuation. Moreover, I disagree that the generative AI cycle is at an unprecedented hype stage, but everyone is entitled to their opinion. Instead, I believe we're likely early in the AI ballgame, possibly around the bottom of the fourth inning, if I may use a baseball analogy. Therefore, Palantir could continue commanding a relatively high valuation of around 50-65 forward EPS estimates in the coming years.

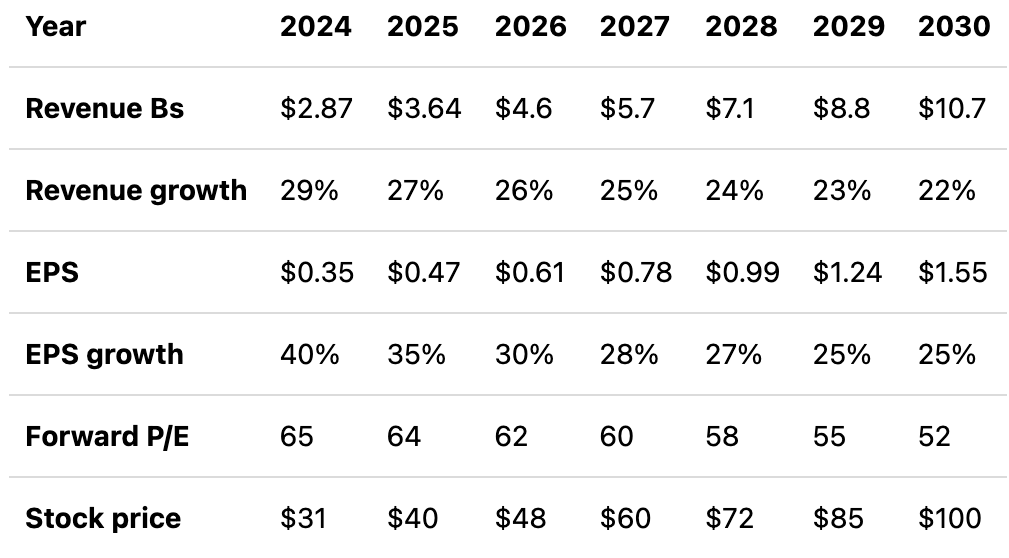

Where Palantir's stock could be in future years:

I'm using relatively modest sales and EPS growth figures to reach my projections. In a slightly more bullish scenario, we could see higher sales growth and more rapidly expanding EPS, leading to a higher stock price by 2030. However, despite my modest to base-case intermediate-term estimates, Palantir's stock could achieve a $100 price tag in several years.

Risks to Palantir

Palantir faces several risks despite my bullish assessment. The first risk is a slower-than-expected economy and the possibility of "higher rates for longer" regime. A slow economy and high rates could impact business spending, hurting Palantir's growth and profitability.

There is also the risk of worse-than-anticipated demand for Palantir's services from the commerce segment. Additionally, government demand could be lower than anticipated if federal budgets get cut.

There is also the risk of increased competition. Other companies could attempt to cut into Palantir's market share. Also, Palantir's profitability could be worse than projected, and in a worst-case scenario, the share price may not appreciate as expected. Investors should examine these and other risks before investing in Palantir.

About The Author

Hey, I'm John, a self-confessed finance enthusiast with a clear goal. My life revolves around numbers, market trends, and economic theories. This website is where I break down intricate financial ideas, explore investment strategies, and share my passion for all things finance. Join me on this journey to unravel the intricacies of the financial world.